Hello,

P2P lending i.e peer to(2) peer lending concept is not new. It is quite simple actually. I want a loan and you have some extra money available. We decide on an interest rate and we execute the contract. Sounds simple, and well versed. In fact, P2P lending has been in existence since the concept of money, interest, repayment has existed.

If this has existed already since centuries, why is it a talking point now a days, is a valid question. The reason is simple, people misutilized the P2P lending ideas. The rich lent to the poor at exorbitant rates, which they failed to repay and led to generations being crushed under the pile of debt, being one of the major eventual outcomes of this practice. This is where the banks stepped in. They provided an organized platform for the lenders and the debtors, while charging an interest as a fee. From the median interest amount, the banks would provide interest at a lower rate to the depositor, to keep the money safe and charge a moderate amount from the loan seeker to provide that loan. An example is the rates of interest a bank charges for personal loan vs the interest it provides for a standard savings account. The difference in the rates, is the bank’s income. Despite the banks being present, the practice of P2P lending in an unorganized way still exists and thrives.

This is where the different NBFC and Fintech companies saw an opportunity. To tap into this unorganized P2P lending market and make it available to the mass. In the Indian market, companies such as Faircent, Paisadukaan, Rupeecircle, etc. have come up, all having their own take at this opportunity.

Brings us to the main question, how is CRED Mint any different? Well, the services it offers are the same as a normal P2P lending platform does. Unsecured loan upto a certain value, 9% interest, easy options to pull your invested money out, etc. but, where it shines is who it chooses to have on the platform. CRED boasts having a stringent entry criteria of 750+ credit score. This easily eliminates a chunk of the population who may pose to be bad debts to a lender. To have a high credit score, you must be crediworthy and to maintain this creditworthiness, it takes financial discipline and effort, which all the members on CRED supposedly exhibit.

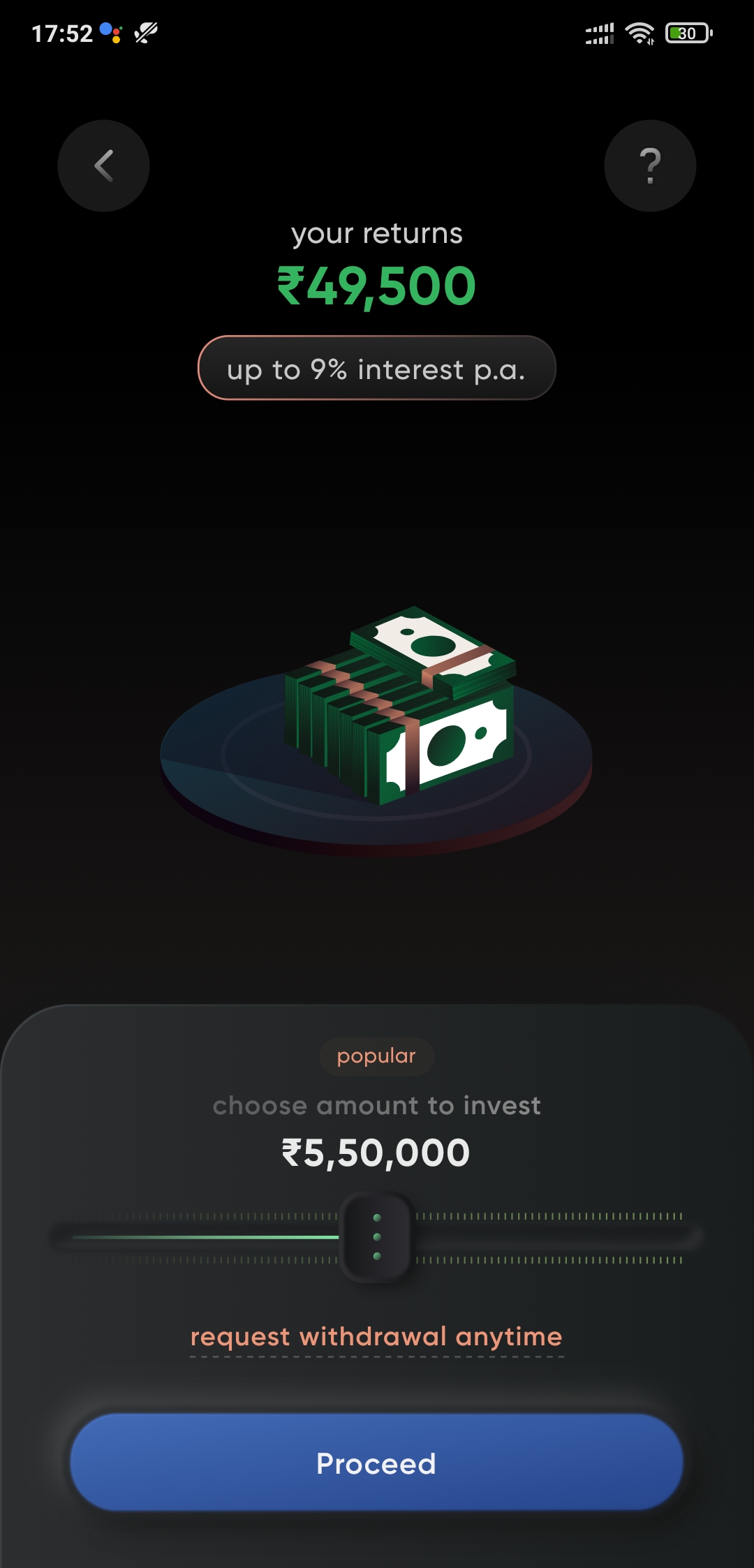

This makes CRED Mint incredibly safe to use as an investor. One cannot look away from the fact that the offered interest is 9% p.a which is incredibly high even if compared to the FD rates available. They do have an entry barrier of minimum Rs. 1 lakh, maximum upto Rs. 10 lakhs as an investor, while as a borrower, I believe the maximum limit is of Rs. 5 lakhs.

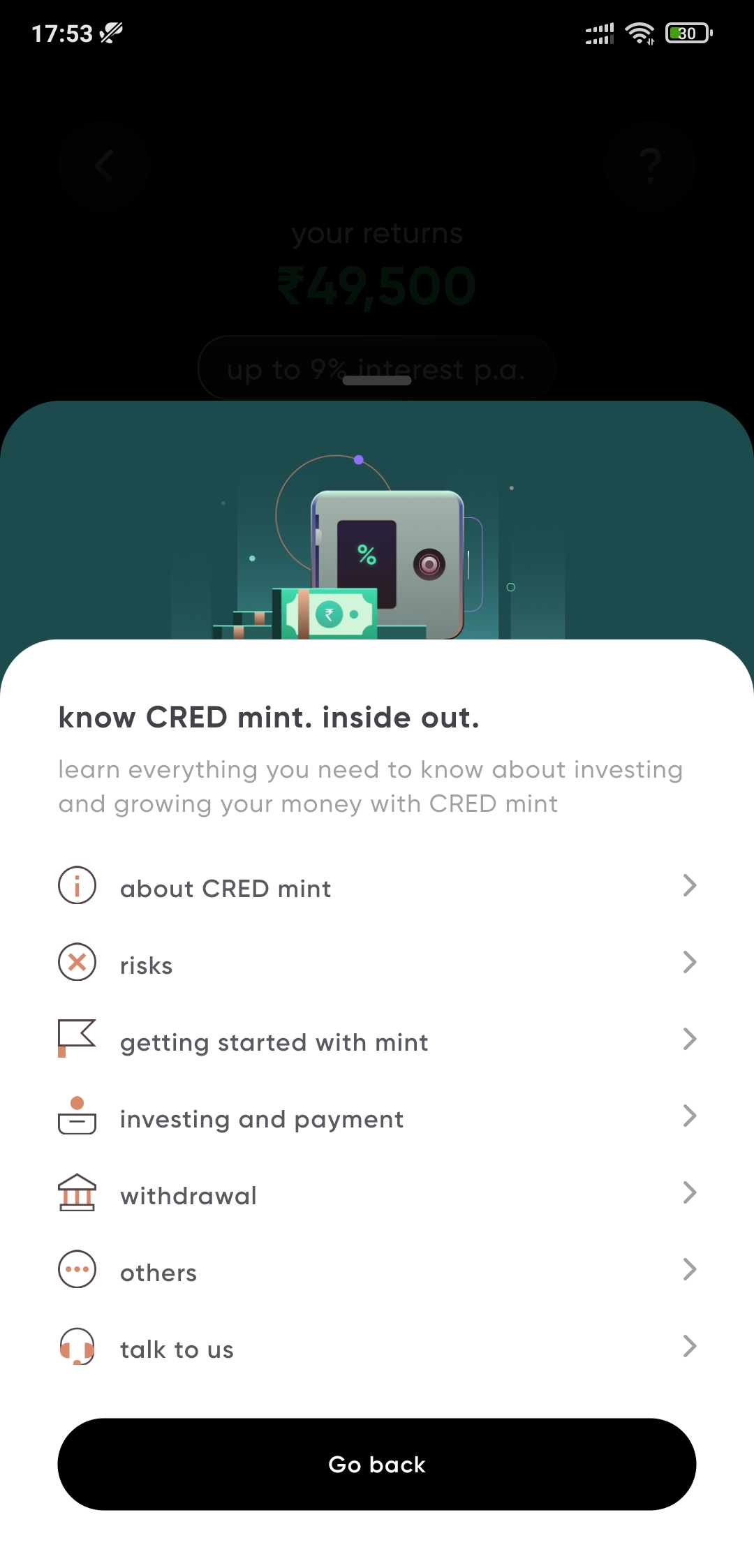

The process of enrollment into CRED Mint is still based on invites as of now and shall be open to the entire CRED community soon. The steps are straightforward and simple to follow. Best part is an entire section dedicated to explain the entire P2P lending process along with a very detailed FAQ.

Have I invested in Mint yet? No, I do not have enough spare money lying about, just yet. But I will invest here soon enough. Should you invest in it? If you have some money to spare and are not risk averse, have a decent enough credit score, yes, you definitely should.

If you would want to get a Rs. 250 voucher when you sign up for CRED, please do let me know in the comments. The referral links stay active only for 48 hours, hence can’t post a permalink here.

Please let me know of your thoughts on CRED Mint’s P2P scheme. To read in detail of the intricacies of P2P lending, this page from cleartax is a great resource. Please check it out here.

Until the next post,

Cheers!!