Art has always been a dance between human imagination and the limitations of our tools. But what if those limitations could be swept away, replaced by a digital brush wielded by the power of artificial intelligence? Enter the world of AI-powered content creation and art, where the canvas becomes a living playground and your creativity knows no bounds.

My recent foray into this realm has left me breathless. Imagine crafting text prompts that blossom into breathtaking images, each stroke on an AI live canvas breathing life into pixels, evolving the artwork in real-time. The ability to experiment with diverse styles, from hyperrealism to abstract whimsy, is a creative playground like no other. This is just the tip of the iceberg; the possibilities for AI in art are as vast as the human imagination itself.

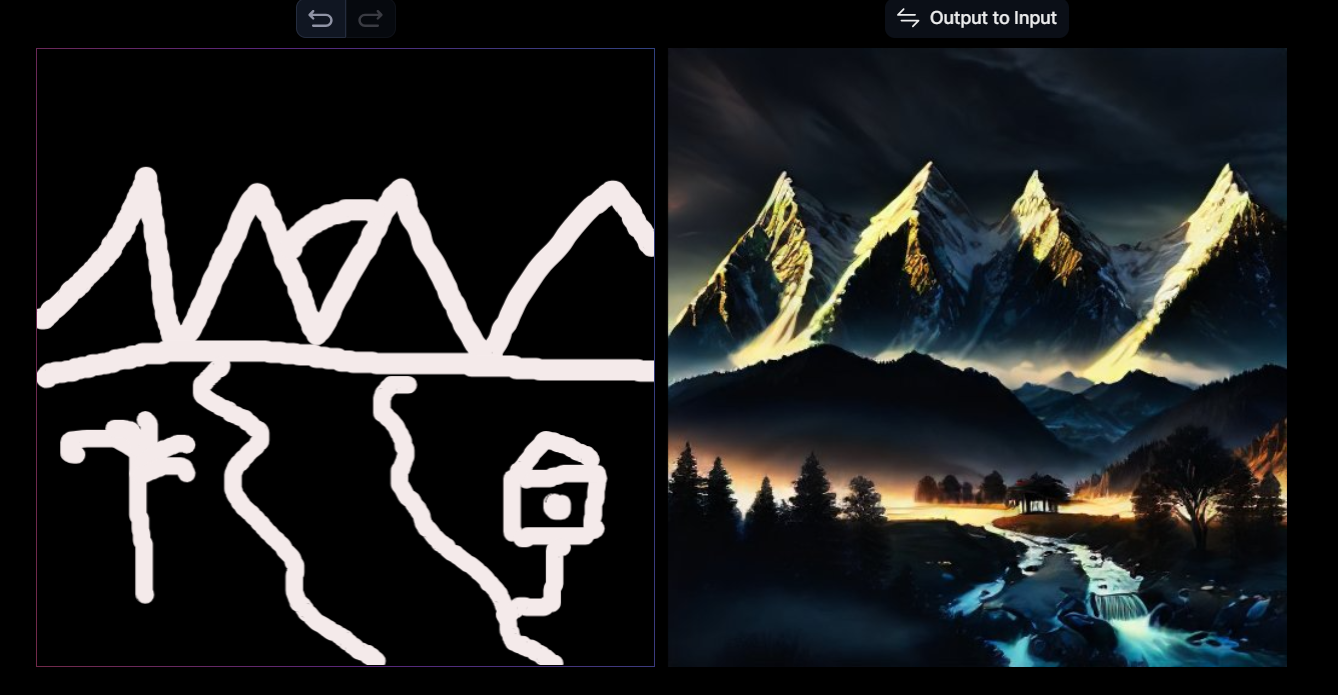

What you see above are just two of the many variations that I created out of a simple sketch and then tweaking various parameters. But this isn’t just about convenience or spectacle. AI can be a powerful collaborator, pushing creative boundaries and sparking new ideas. Imagine a world where an artist’s brushstrokes are amplified by AI algorithms, suggesting unexpected color palettes or surprising forms. This isn’t about replacing the artist, but rather about creating a symbiotic relationship where humans and machines co-create, pushing the boundaries of what art can be.

Of course, this new frontier comes with its own set of questions. How do we ensure AI art remains authentic and meaningful? How do we prevent the homogenization of creative expression? These are critical issues that require careful consideration and open dialogue.

Yet, the potential of AI in art is undeniable. It’s a democratizing force, making artistic tools accessible to anyone with a spark of imagination. It’s a catalyst for innovation, pushing the boundaries of our visual language. And it’s a reminder that the human spirit of creativity will always find a way to express itself, even in the face of the most advanced technology.

Before we part, it is important and imperative to show you, just how much amazing AI is. The photo below is a screenshot from the AI website that has been respobsible for creating these amazing images.

So, the next time you feel the urge to create, don’t be afraid to explore the world of AI. Grab your virtual brush, let your imagination flow, and see where the pixels take you. The future of art is being painted right now, and you, my friend, are an artist in this digital renaissance.

I would love to hear about your forays into the land of AI Art in the comments below! Let’s spark a conversation about the future of creativity.

With the end of the collaboration between Intermiles and ICICI bank, the Visa-powered Intermiles card from ICICI has now been discontinued. So, my search for a travel-centric credit card began once more.

This time, my needs were simple. The card should provide reasonable returns in the form of points or cashback, provide lounge access, and have a low forex markup charge. Having a low joining and annual charge was a good feature on top. During the search, it became clear that most of the cards have been devalued and lounge access has become a rarity for the cards that are not in the Premium or Super Premium range.

Since I was not willing to spend a lot on the charges, the search continued, until I found the Scapia card.

This card has zero joining fees and zero annual charges, issued by Federal Bank. It is available on the Visa platform. Along with it being an LTF (lifetime free) card, the USP is that it has ZERO FOREX MARKUP charge. So, when making payments in a foreign currency, we do not incur any markup. You pay the conversion amount, that’s all.

Rewards are in the form of Scapia coins. For every transaction that is not on travel, we get 10% Scapia coins and for travel-related transactions, it is 20%. Forex payments do not provide any points though. And the points accumulated can be redeemed only on their app which is completely travel and hotel booking centric. The app has options of flight and hotel booking and the rates are quite competitive. A thing to note is that this card offers unlimited lounge access but with a condition. The condition is that there must be spends of at least ₹5000 in the previous month. Considering that this card can be used like a regular card and the options it provides are not atrocious, spending at least ₹5000 in a month and gaining the option of unlimited lounge access across India is quite nice.

The application process for the card is a simple and straightforward one. You download the app on your phone, fill in the details, accept the terms and conditions after reading them carefully, take a selfie, and done. Your virtual card becomes ready for use immediately and can be used for online payments. The physical card arrives a few days later in a funky box. There is a booklet with the most important terms and conditions (MITC), some stickers, and the card itself. Neat packaging I must say.

In the app, they have a gamified target spend roster known as Scapia Heist where based on the amount and number of spends you get badges and they lead up to more points. It’s a nice touch in the app. Various deals in Dining, Travel, Fashion, Health and Wellness, etc. are applicable to the card and accessible through the app.

A group of customers who would enjoy having this card is the bloggers and other content creators who may be active on international platforms such as WordPress where the payment is in USD. For people like these, this card would save quite a bit of money and might serve as quite an attractive proposition as well.

Overall, I feel this card is a good card to have especially if you travel quite a bit and are looking for a zero forex markup card, without breaking into the premium and super premium segment. Give this card a shot, it would be worth the effort.

The following article aims to understand how much it costs to begin investing in the US Stocks market, from the perspective of a general salaried individual. The assumptions here are that the reader understands the stock market and is interested to invest in the US market. Also, the investor understands that there are tax implications, exchange rate fluctuations and is savvy enough to test the waters on their own.

Investing in the US Stock market has always been quite lucrative for the retail investors of India thanks to the options of fractional buying and the advantage of the higher exchange rate of the US Dollar against the Indian Rupee. An investor who might have invested $200 worth of US Stocks at about ₹50/$, assuming zero share price movement, would have a portfolio appreciation of about 64% in the current times without having to do anything at all, simply because Rupees depreciated and became ₹82/$ i.e an investment of ₹10000 becomes ₹16400. Fractional buying, as mentioned earlier, is also an interesting thing. In the Indian stock market, you cannot buy ₹500 worth of MRF’s stock because here the minimum number of stocks has to be an integer, meaning, a minimum of 1. So, your minimum investment in MRF has to be ₹88320 (as of 14-Feb-23). This is an entry barrier for a lot of retail investors. On the other hand, you can buy ₹500 equivalent of Tesla stocks and begin your US stock investing. The easiest way to get benefits of the US market in providing some risk coverage to your domestic portfolio is by investing via mutual funds which also have US funds. It is simple and hassle-free. It functions just like the normal funds, just that they invest in a US fund, generally owned by the same company.

But, if you want to take charge and invest personally, there are a few available options. The traditional way exists by opening an account with international brokers and then proceeding as usual. Brokerages are generally high and there might be a few restrictions in place. The alternative is to use the apps such as INDMoney, Groww, Vested etc. These apps tie up with banks and use their DEMAT accounts for investing, or with US brokers who open an account on your behalf and the investment begins. One of the biggest marketing flex that these apps have is that they are zero commission platforms. That means, the apps do not charge you brokerage for the trades. While this is lucrative, charges exist for the withdrawal of your fund within certain limits. So, what is the minimum cost incurred to begin investing? Let’s take two examples and try to find out. We shall be considering Vested and INDMoney.

Vested has zero sign-up charges, but it needs for you to have a DEMAT account with Axis securities. That costs ₹499 initially and then at least ₹750 per year, then on. Beyond this, money has to be transferred from your bank to the US broker’s account. Each transaction costs a minimum of ₹1000 in transaction charges, ₹500 in SWIFT charges and 18% GST. So, for the 1st transaction, it will cost about ₹2000. This is without considering the bank’s exchange rate.

INDMoney, on the other hand, creates its own DEMAT account using KYC documents and then all you have to do is fund your US account. There too the charges are similar, except for the initial ₹499 as account opening fees. Here too, you are at the mercy of the bank’s rates to be able to transfer money from India to the US.

In my limited search, I found HDFC bank to have the least transaction charges. Beyond this, most of the banks range in around ₹1200-₹1600 per transaction. Something that is to be taken into account is that a big portion of the transaction fee is a fixed charge. So, whether you remit ₹5000 or ₹50000, the transaction fees would be very similar, with only the tax part changing. So, it is smarter to move a chunk of money and then invest from the chunk over a period of time, rather than affecting multiple smaller transactions.

In the latest budget proposal, there is a clause suggesting the implementation of a 20% TDS on foreign remittances, irrespective of a threshold. This TDS would be deductible against the income tax of the individual, but it is still a bit of “stuck” money. So, if you are planning to invest in US Stocks, the time seems quite ripe for the same.

In case you consider INDMoney, you may use the following referral code: KAU734U3IND I hope I have been able to shed some light on the costs involved in beginning your US Stock Investing journey. Happy investing.

On the 1st of February, 2023, Ms N. Sitharaman, the finance minister of India, delivered the last full budget before the term of the current govt. ends and general elections occur, expectedly, in May 2024. There were many expectations out of the budget from various groups of people and institutions, some have been met, some exceeded, while some have fallen short as well.

This post is not for the analysis of the entire budget, but rather of a very particular section, that affects salaried countrymen like myself, the Personal Income Tax.

With the proposal for the new tax regime for 2023-24 (hereafter mentioned as the new regime), discussions have come aplenty as to how much tax would be saved and how it shall spurt the growth of the economy and so on. It is beyond doubt that the disposable income at the hands of the salaried employee will increase, let’s take an example below.

For an employee, earning a gross income of ₹12,00,000, the income tax, as per the new regime comes to be ₹85800. For the same employee, under the old tax regime, considering the standard deduction of ₹50000, professional tax of ₹2400 and assuming HRA exemption of 15% of gross, the taxable amount becomes ₹967600, which attracts a tax of ₹110261. A difference of ₹24461, is definitely not a small amount. One must note that here we are considering that there are no tax-saving investments made. No 80C, no 80D, nothing. We can summarize that by following the old regime, the employee would have a monthly income of ₹71445, whereas the new regime would provide ₹92850, a clear ₹21000+ difference. At a glance, this is quite amazing. Higher disposable income will invariably translate into higher consumption, which in turn will lead to better economic scenarios.

On the flip side, we must note that most of the exemptions that the old tax regime offers are tied to a certain security for the future. The sections 80C, 80CCD, etc. are aimed towards savings for the future, in the form of PPF, ELSS schemes, Sukanya Samriddhi schemes or NPS. So, for people who are still not too concerned about future plans, even for the sake of avoiding tax, there are avenues for savings. In the new regime, there is no such obligation. Rather now, one must be careful as to not spend all the money away on luxuries, rather than saving for future security. The fact that just because there are no exemptions anymore, does not mean that the need for insurance schemes shall vanish. Worse still, now one has to buy the schemes, as usual, but not be able to claim any tax rebate, if following the new regime.

Reimagining the above example, but this time, we consider that along with the deductions considered earlier, there is also ₹250000 worth of savings done in the form of 80C, 80CCD (NPS) and 80D schemes. The resultant taxable income becomes ₹717600. Calculating the tax on this, as per the old tax regime, we obtain a payable tax of ₹58261. Calculating further, we obtain a monthly disposable income of ₹59311. While this is about ₹12100 less than the disposable income obtained if no savings are done, savings towards future security is being done. The point to note is that the new regime shall provide an increase of ₹33500 per month as disposable income. For an entrepreneurial person, it is an outright boon and it opens up growth opportunities.

Concluding the above views, we realize that the new regime will put more money in the hands of the individual, provide greater control and above all, entrust a lot of responsibility. As a follow-up to the budget, there should be more widespread awareness sessions about the various investment schemes, so that the people who opt for the new regime can utilize the money fruitfully.

This move, by Ms Sitharaman, might very well prove to be a turning point in the history of the country where the increase in the involvement of the salaried class in the investment market is remarkable or it may be the beginning of a downward spiral where unnecessary spending takes precedence over future planning leading to eventual misery and woe.

To end, I realise that people who understand their money matters properly, can control their finances well and believe that they can take care of the situation on their own, they must choose the new regime. The ones who are not too sure about their capabilities and would like to play it safe should invest as much as they can and take advantage of the old scheme. Finally, in my opinion, no one should opt for the old scheme if not keen on investing in any of the tax saving instruments currently.

The excel sheet used to make the calculations and come to the results is linked here. Please feel free to use it to compare your own tax liability. I am not a “Tax Expert” but I do fill my own ITR, am sure that counts 😊 The cover image has been sourced from Shutterstock via Google. I do not own any right to the photo.

I will be thrilled to read your thoughts on the report and am sure, I shall learn from your perspectives as well. Cheers!

The basic definition of Art is that it is a means of expression by intelligent beings. The means of expression can be singing, dancing, drama, literature, music; the list is endless. Since the time when the first human could express their surroundings, they have done so. In the form of cave paintings and sculptures, and one can agree that when we mention art, the first thing that comes to our mind is either a sketch or a painting.

Up until very recently, the ability to create art was natural. I will elaborate. Natural, in the sense that it had to be an intelligent being who was creating the art in the form of painting, sculptures, songs, etc or it would occur spontaneously in nature, such as the geometric shapes we see in the snowflakes or in hail, the patterns formed by flower petals etc. But now, since the last few years, there exists a means to create art, quite literally using plain text words. I am referring to the use of AI to create art. Now, we can type in a few words to describe our imagination and Voila! we have our artwork ready.

Let me show you some examples!

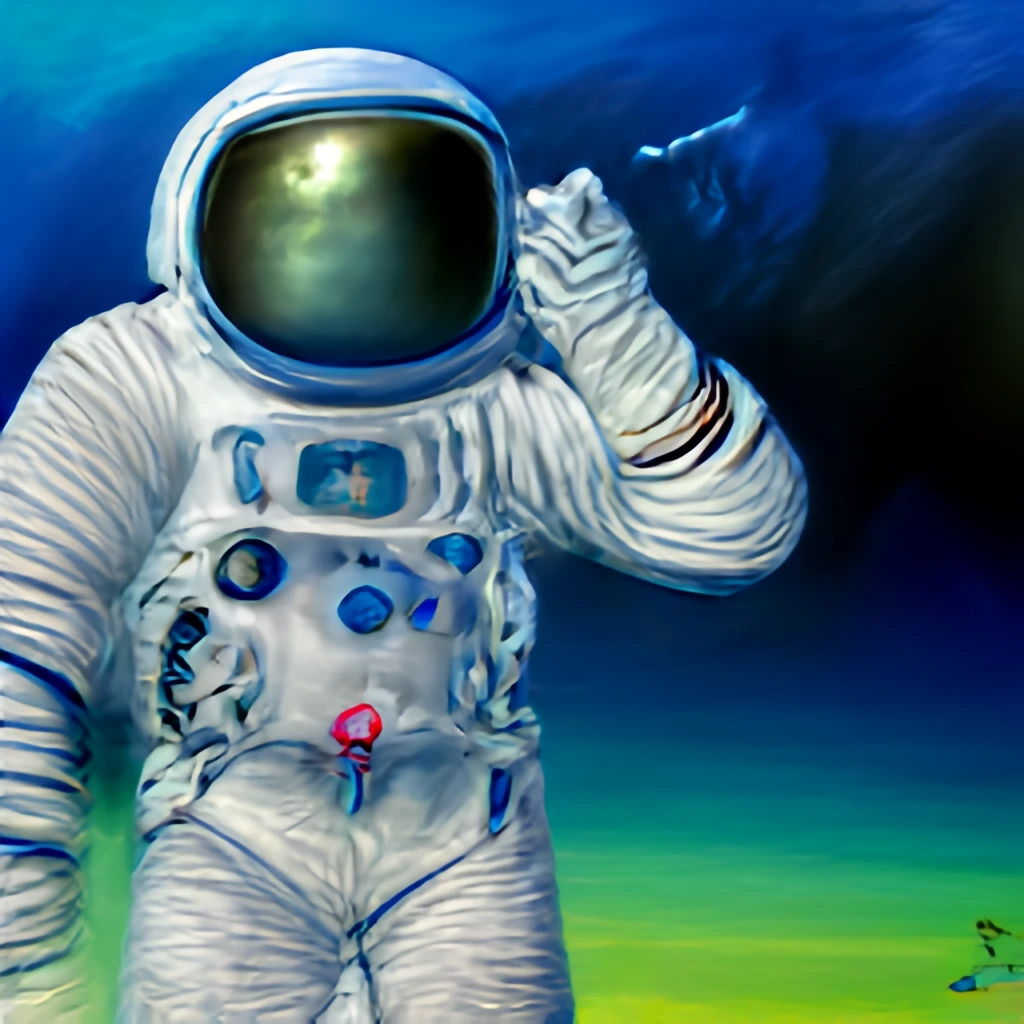

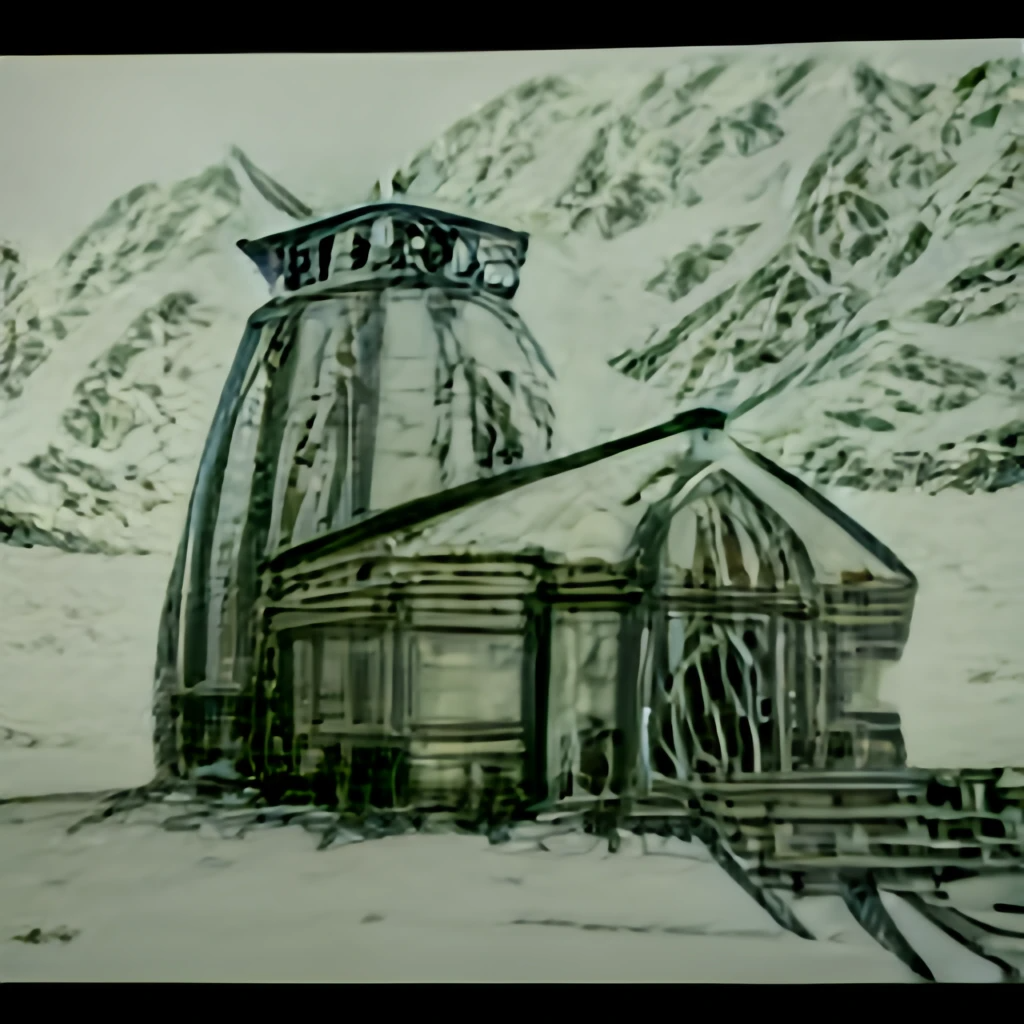

These images you see here, I can claim to be the brains behind the prompt that produced them, but the creator’s credit goes to the AI.

The way this works, on the front end at least, is as the following. We conceptualize what we want, the weirdest, wildest ideas, in the most vivid detail. Write it down on the available prompt of the software/app/webpage. Hit the create button and choose the output from the list of generated images. Of course, behind the scenes there exist many algorithms to decipher the text and their understanding, then generate the images which fit the prompt. One can also describe the type of output expected, such as photorealistic, oil painting, pencil sketches, etc. And, it can be as weird as your imagination as well.

Better still, these AI-generated images can be made copies of and sold as framed paintings, printed on T-shirts, even as NFT. So, all you need now, to become a celebrated artist, is to have a vivid sense of imagination, a powerful AI tool and some time to spare.

These images have been created by me using the website Craiyon and via DALL-E. Do check them out and post your masterpieces.

I was born in 1991 and neither of my parents, during their years of career has had a credit card. So, at the first opportunity, 26 years later, I promptly obtained one. For a lot of people in the middle class, my generation is the first one which takes the plunge into the world of rewards, cashbacks, due dates and balance transfers. Almost every bank we know of, issues a credit card and each has its own pros and cons.

Amongst the cards available to be issued based on applications, AMEX cards are one of the most desirable ones. So, yet again, upon realizing that I was eligible for one and would be able to use it fruitfully, I applied and obtained one. The prime objective was to experience the enigma around AMEX cards, the rewards programmes and to be honest, the slight feeling of pride from the second glance the card receives as you hand it out to be used.

In the post ahead, I shall discuss some of the basic questions that I had asked around and hope that it’ll help you too. The discussion aims to cover

Types of cards – Debit/Credit/Charge

How AMEX is different?

Eligibility and why you should get one

The rewards programme

Pros and Cons as experienced by me

How to get an AMEX card with no annual fee

Let’s begin!

Types of Cards – Debit/Credit/Charge

These three are the major types of cards available easily to any customer.

The Debit card is linked directly to your bank account. There are daily transaction limits on the card and you can, technically, spend as much as your balance is in the linked account. In India, for most debit cards, a daily transaction limit of ₹50,000 exists. Debit cards are given out as a part of the standard kit while you open a new account in the banks. These are generally free of charge or a minimum yearly charge for account maintenance is charged.

The Credit Card (CC) is not linked directly to your bank account, in a manner that what you spend on the credit card will not dent your bank balance immediately. Every CC comes with a limit of sorts, which is the maximum expense that you can incur on that card. There is a fixed number of days in which you must repay the CC account, which varies from 30 to 51 days in general, which is known as a credit cycle. The limit of the card is dependent on your income, spending habits, CIBIL scores; simply put how reliable you are that you shall pay the money back, from the bank’s point of view. This causes the limit to vary wildly. For me, I have had cards where the limit varied from ₹18,000 to ₹2,50,000, and the limits keep on changing over time. Also, in case you are unable to pay your dues on the due date, there is an interest that is charged for every day that you delay settling the due. These cards can have loads of rewards attached to spending goals and may have annual charges for them.

What about the needs of high spend groups? Having a limit on their spending is not suitable for them, so there comes the third kind, Charge Cards. These cards are meant mostly for people who require virtually unlimited spending power while being able to repay on a fixed date. Charge cards mostly include an uncapped spending limit, loads of reward points and an annual fee. The prime point for a charge card is that you must pay the due on the day of the statement. There is no free credit period as such for these cards. So, these cards are best suited for business purposes, where transactions are settled on a fixed date basis. In case there is a fee default, it gets reported to the credit bureaus and has major negative effects on the cardholder’s credit ratings and in turn to his/her credibility in the eyes of the bank. So, if you are sorted with your finances, have the requisite control needed and do not mind paying the annual fees, the rewards of a charge card can be very alluring indeed.

Some of the debit cards I own!

How is AMEX different?

The biggest difference is that AMerican EXpress (AMEX) is not a bank. It is a credit card issuing agency that issues its own cards and has tie-ups with most major banks of the world. So, you can not have debit cards from AMEX, though you might have AMEX affiliated ones, similar to the VISA or MasterCard or RuPay ones that we see commonly. There are prepaid AMEX cards too. So, what difference does it make for you and me? The answer is, to obtain an AMEX card, you’ll have to either apply for it or be invited to its membership. Of course, most major banks of the country have credit cards that are AMEX affiliated, but they are still not technically AMEX cards.

My AMEX card

Eligibility and Should You get one

The eligibility criteria for AMEX cards vary according to the cards themselves but are quite stringent as compared to the cards from other banks. An annual salary over ₹5,00,000 with a CIBIL score of 750+is generally recommended for being eligible for at least one card. We must remember always that being eligible does not mean that you must apply for it. You must have a clear idea of why you want the card? Is it for the benefits and rewards or just use it as a status symbol? Are you ready to pay the annual fee for it (You can get it for free too you know! Check the last point 😉)? Would you be able to utilize the card fruitfully? If you can justify yourself on these questions, then you should go ahead with it for sure.

My reasons to get the AMEX card were driven by the zest to try out the rewards being offered by AMEX. Since I had already been using my existing cards for most of my expenses and shifting to the new AMEX card was neither difficult nor have I had to go out of my way to spend differently.

The Rewards Programme

Let’s be honest, we choose credit cards based on the rewards they provide. Most have some sort of a cashback in place; be it as points, statement credits or miles. These rewards can be redeemed for physical things such as discount coupons, electronics, holidays, flight tickets and even cars. And this is what entices us ultimately, the value for return.

For AMEX cards, this value is high. They have multiple reward programmes running at a time which can be used quite interestingly often. As of now, besides the discounts being offered on the card in dining, shopping and such, they have spend based rewards at 18k and 24k points. Of course, you can redeem your points for statement credit monthly, but that is a sheer wastage of points.

Let’s take a quick example to see how using the AMEX card cleverly can be useful for us.

Assumptions:

The card is AMEX MRCC (Amex Membership Rewards Card)

The monthly expense is at least ₹20,000. This is not difficult if you include rent payment via credit card.

You have signed up for the spend based rewards programmes.

Scenario:

For the MRCC, you get 1 point for every ₹50 spent (some exclusions exist, such as utilities, fuel, etc.).

Spending ₹2,40,000 in a year provides you with 4800 points only. That is honestly very sad.

But, if you make at least 4 transactions of ₹1500+, you get another 1000 points. Assuming that is being done, the new total becomes 16800 points.

Signing up for a spend based reward programme, where if you spend more than ₹20,000 in a calendar month, you get another 1000 additional points. Assuming that is being done too, now, the final total becomes, 28800 points.

Now, with 28.8k points, you become eligible for both 18k and 24k rewards.

The 18k rewards has Taj vouchers, Amazon gift certificates, statement credits etc, while the 24k rewards has Tanishq vouchers too along with Taj vouchers and Amazon gift certificates. You can choose from these at your will. Apart from redeeming the points as rewards on AMEX, you can choose to convert some of them to air miles and redeem flight tickets too.

So, you see, if used cleverly, AMEX credit cards can be quite useful. It is not that these offers are available only for AMEX, but rather every card comes with its own sets of rewards. Some research helps.

Pros and Cons As I see it

The Pros and Cons of an AMEX card are as varied as the person using it. For me, the rewards were more enticing than standard cashback, while the main disappointment has been the non-inclusion of the MRCC in the airport lounge programme. I do not fret much about it though, since I have other cards which provide airport lounge access, but if the MRCC provided the same, it would have been nicer. Not having to pay annual charges offsets the disappointments greatly.

How to get an AMEX card for free

One thing we must understand is that the reason AMEX and other better-than-the-rest cards can offer the rewards is that they all have annual fees. In the case of AMEX, the MRCC and the SmartEarn are the two cards that have the option of fees waiver based on the spend.

SmartEarn is aimed towards the ones who want to have an AMEX card in their wallet mostly to feel premium about owning an AMEX card. It has the least entry requirements and does not have a lot of value in terms of rewards other than accelerated points accumulation.

This card has an annual fee of ₹495 + taxes which is waived off upon spending more than ₹40,000 in the previous billing year.

The MRCC on the other hand is aimed at people who want to enjoy the fruits of their expenditures but are not willing to spend a lot though. It misses out on lounge access, golf club memberships etc, but offers you possibilities to stay at Taj or gift yourself/ your beloved Tanishq items.

This card has a first-year fee of ₹1000 + taxes and an annual fee of ₹4500 + taxes. But, if you use a referral code, such as the one below, the first year fee becomes Nil and the annual fees come down to ₹1500 + taxes. In fact, if you use the card the way I have mentioned in the example and use my referral code, that’s how you can get your AMEX card for free.

Update:

Please note the exact charges would vary from card to card and kindly check for the latest MITC for the card on the AMEX website. As of February 2024, you will get the first year free, saving you ₹3500 and 2000 points bonus.

To end, I shall say that it is time that we begin using credit cards for our daily expenses. It promotes healthy financial discipline and improves your credit score. The credit score is an important tool to decide at what rate you shall get your loan from a bank. Mostly, higher credit score holders get better terms for their loans and the chances of rejection are minimized greatly.

Feel free to reach out to me with your doubts and questions, I shall be happy to help solve them 😊

The RBL Zomato Edition card has been discontinued by the bank and has been replaced by a RBL Shoprite credit card. The Zomato Pro and Zomato Pro+ schemes have also been ended by Zomato and the older Zomato Gold has returned. For the ones who would order regularly from Zomato, this card was a nice one and it shall be missed.

No, it is not just a clickbait headline.

Zomato, the leading food aggregator service platform has come up with a unique proposition, in collaboration with RBL Bank in India, targetting their best-known customers, The Foodies! They have a credit card, Zomato Edition and for as long as you own the card, Zomato Pro shall be free to your account. The card has no joining or annual fees and offers quite interesting cashback, redeemable on Zomato. The proposition seemed nice, so naturally, I applied for it.

The application process is simple. You log in to the Zomato app, head over to the tab that says, Money. There, you’ll find the option for a Zomato wallet and Editon. Selecting Edition will take you to a signing up page, where you provide consent of application, addresses, etc and then upload the documents. The KYC with RBL bank happens over video call and is smooth. And then, in about 2/3 business days, you have the card with you.

Zomato Edition box and its contents

The offers that were provided to me can be seen on the below screenshot of the email.

Benefits of the Zomato Edition Card

Basically, we have a card, which is lifetime free. No annual charges. VISA Card, so accepted globally. Has a decent credit limit. And offers cashback in the form of Zomato credits. You can choose how much of the cashback do you want to use as Zomato credit at a particular time. And, Zomato Pro for as long as you hold the card. An absolute win-win situation for anyone who uses Zomato to order food.

I honestly do not see any downsides to this card, that should deter anyone who uses Zomato, from ordering this card. Tell me your thoughts on this in the comments below!

Yesterday I began trading in options, and today, I have made my first loss. This is the story of my early mistakes so that you do not make them. Egged on by the videos of Rachana Ranade ma’am, P R Sundar sir and Ankur Warikoo sir, I too decided that now the time is ripe to try out my hand at options trading. To begin, I do not have a lot of bankroll at my disposal, so options buying, that too, out of the money. By the way, if you want to know what options are, or what OTM, ITM, ATM means and other nuances of trading in derivatives, check out the videos from the teachers I mentioned earlier, you’ll get the hang of it. So, with a limited kitty of ₹6000, I opened an account in Zerodha. Yesterday, I put in my first options trade, cautiously. I did not put a stop loss in place but then the market was bullish all the way. As soon as I made about ₹100 profit, I bailed out. Of course, way too cautious I must say. And by the end of the day, had I persisted, the profit would have been about ₹1500. I felt a bit silly. So, last night, I made the plan. Assuming the market opens in the green, I’ll enter a buy position quickly in the morning and then hold on to the position for the day, or until I see a loss of a maximum of ₹500 (around 10%). Today morning, as the markets opened in the green, I put my plan to action; rather, tried to put it into action. The first hurdle, the stop loss. In my understanding, if I want to buy a position at a certain value, I enter that as the limit price. The stop loss is where I don’t want the price to fall beyond and limit my losses. So, that value must go in the stop loss value. But this is not how Zerodha functions. No matter what I do, Kite (Zerodha’s trading platform) would just not let me enter the stop loss that I want, rather it wants me to enter a price above the last traded price. After fighting with the system for some time, I just put in values at market price and sent out an order. The stop loss was about 50p below the buy price. In about 10 minutes, I was stopped out and exited the trade. Now, in an options trade, the ticker does not necessarily go down by 50p each time. It might drop by quite a value before the stop-loss kicks in. So, I have a loss of about ₹200. Still within my budget for the day. I tried again, this time, I raised a ticket with Zerodha, explaining what I thought should be stop loss, and sent out another order. This time I got stopped out after about half an hour. Another loss of almost equal amount. Then I found out the correct way to do it. You enter a buy position. Then, you put a sell order, with the stop loss that you feel is correct. So, this works as your safety net. Upon having this revelation, I tried once more. This time, the order was correct, and based on my expectations, I put in a stop-loss order. My order got completed with a loss of another ₹250 in the next 20 minutes. And I thought to myself, enough for the day. The market is not good, let it be. All of this happened by about 10:30 – 11:00. But then, the itch remained, and at about 13:00 I opened the site again and imagine my amazement, to see the prices, which had made me lose about ₹500 already, are soaring. I mean, had I remained in the last loss-making position, I would gave been seeing an upside of at least ₹600 at that time. So, what did I do? What any normal person does, I put in another trade. This last trade, I am tracking it. Tenaciously. Increasing the stop loss gradually so that I get maximum profit out of it, but then, the earlier trades have done so much damage that despite being up in double-digit percentages, the last trade will not be able to make an overall profit. Anyway, what is the learning from my ordeal of the day? Have patience. And read the manuals. I was ready to deal with a 10% loss right at the beginning and had that been my initial stop loss, in the very first trade of the day, I would not have been stopped out 3 times and would have enjoyed quite a bit of profit. I know for sure that this will not be the last time I am making a loss in a trade, but then, now I know how to put the stop loss in place correctly. Thanks for being my reader today. I hope you have a nice trading session ahead. Cheers and have a nice day!

P2P lending i.e peer to(2) peer lending concept is not new. It is quite simple actually. I want a loan and you have some extra money available. We decide on an interest rate and we execute the contract. Sounds simple, and well versed. In fact, P2P lending has been in existence since the concept of money, interest, repayment has existed. If this has existed already since centuries, why is it a talking point now a days, is a valid question. The reason is simple, people misutilized the P2P lending ideas. The rich lent to the poor at exorbitant rates, which they failed to repay and led to generations being crushed under the pile of debt, being one of the major eventual outcomes of this practice. This is where the banks stepped in. They provided an organized platform for the lenders and the debtors, while charging an interest as a fee. From the median interest amount, the banks would provide interest at a lower rate to the depositor, to keep the money safe and charge a moderate amount from the loan seeker to provide that loan. An example is the rates of interest a bank charges for personal loan vs the interest it provides for a standard savings account. The difference in the rates, is the bank’s income. Despite the banks being present, the practice of P2P lending in an unorganized way still exists and thrives.

This is where the different NBFC and Fintech companies saw an opportunity. To tap into this unorganized P2P lending market and make it available to the mass. In the Indian market, companies such as Faircent, Paisadukaan, Rupeecircle, etc. have come up, all having their own take at this opportunity.

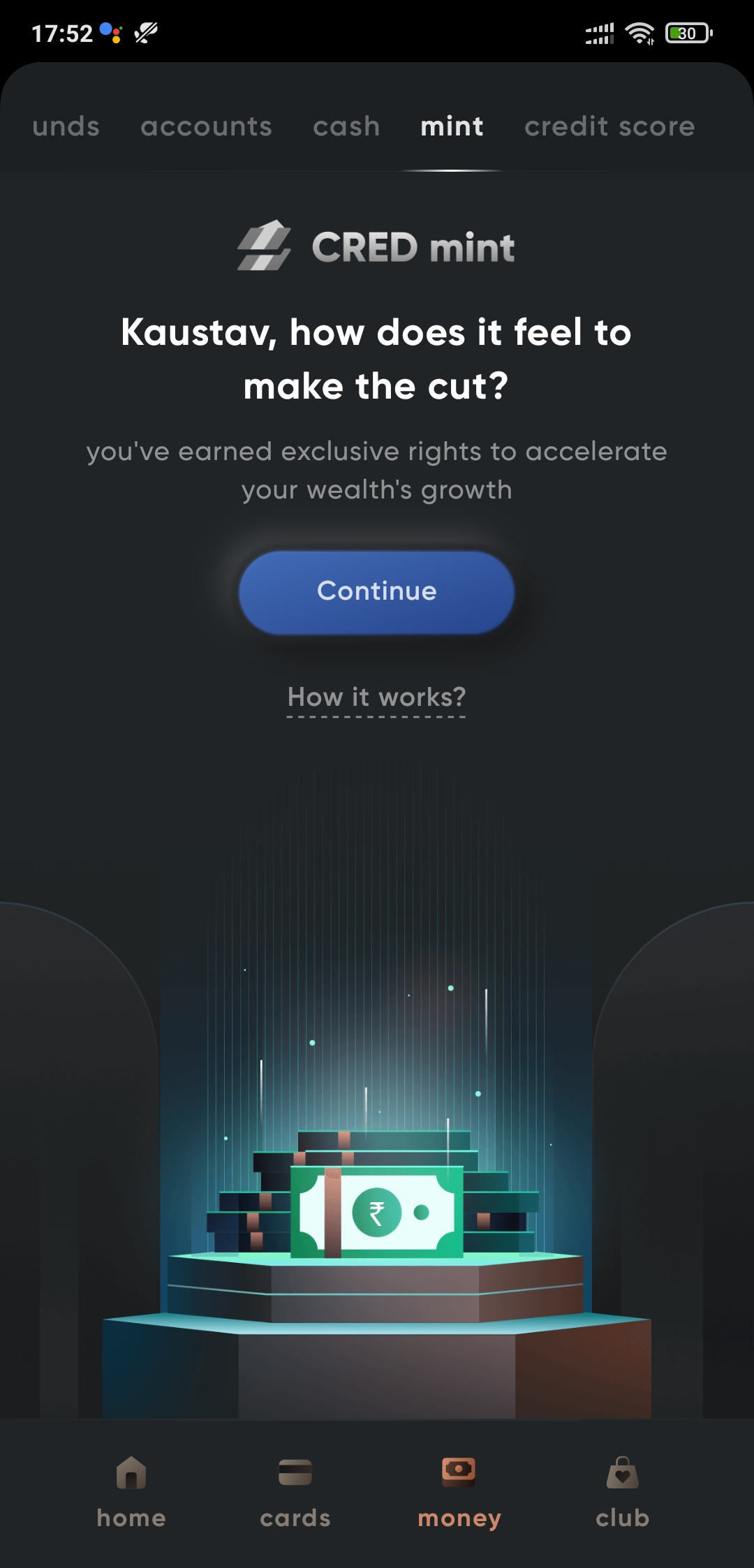

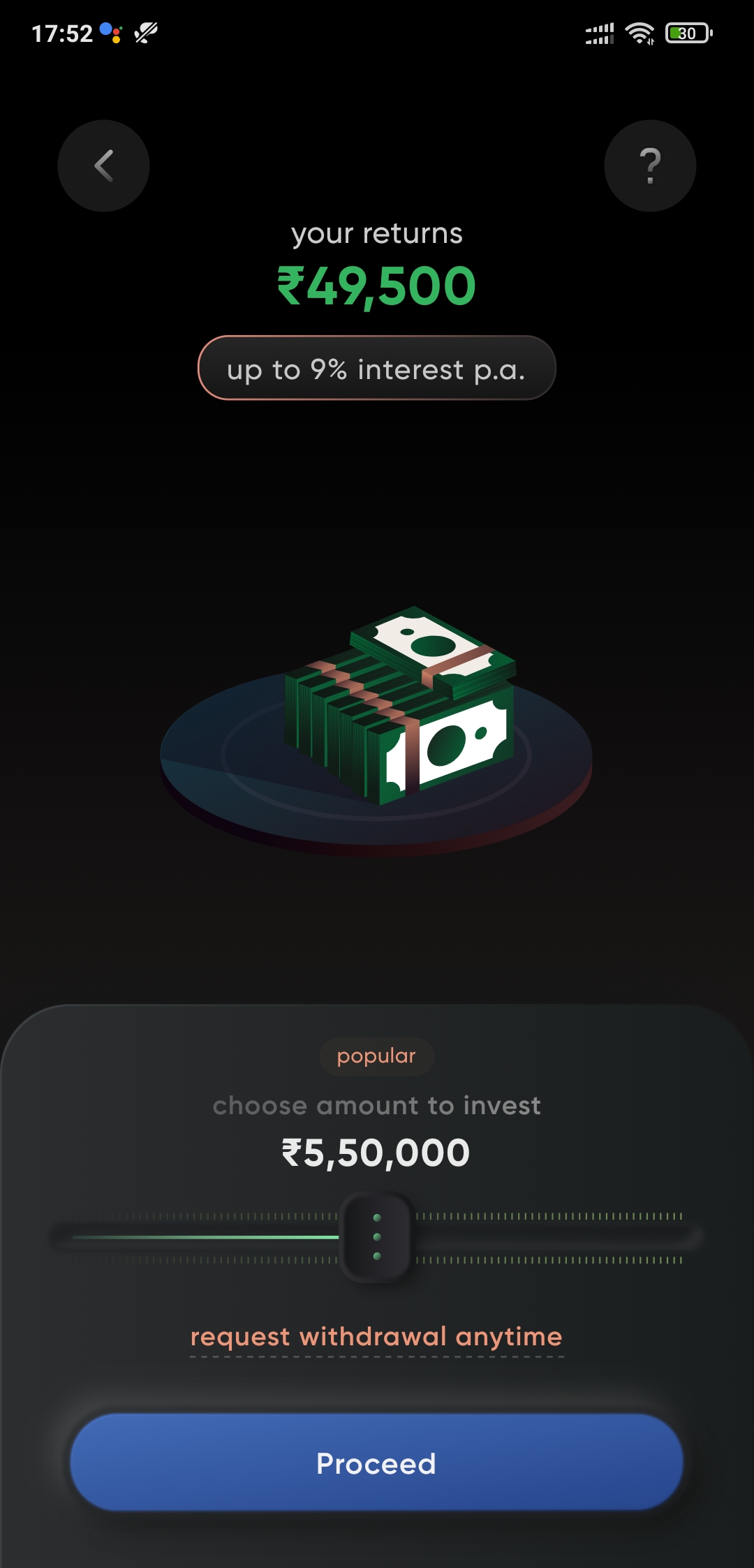

Brings us to the main question, how is CRED Mint any different? Well, the services it offers are the same as a normal P2P lending platform does. Unsecured loan upto a certain value, 9% interest, easy options to pull your invested money out, etc. but, where it shines is who it chooses to have on the platform. CRED boasts having a stringent entry criteria of 750+ credit score. This easily eliminates a chunk of the population who may pose to be bad debts to a lender. To have a high credit score, you must be crediworthy and to maintain this creditworthiness, it takes financial discipline and effort, which all the members on CRED supposedly exhibit. This makes CRED Mint incredibly safe to use as an investor. One cannot look away from the fact that the offered interest is 9% p.a which is incredibly high even if compared to the FD rates available. They do have an entry barrier of minimum Rs. 1 lakh, maximum upto Rs. 10 lakhs as an investor, while as a borrower, I believe the maximum limit is of Rs. 5 lakhs.

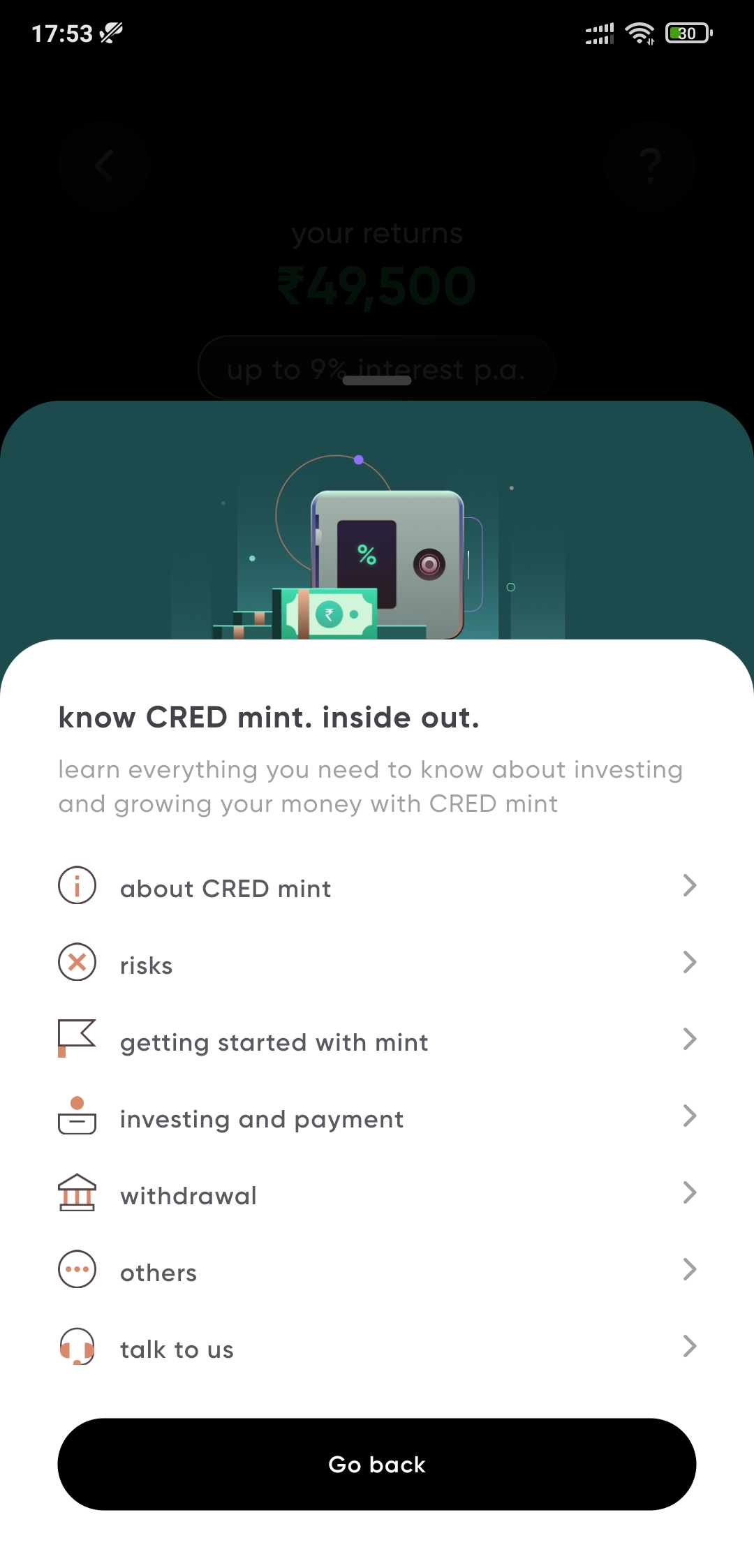

The process of enrollment into CRED Mint is still based on invites as of now and shall be open to the entire CRED community soon. The steps are straightforward and simple to follow. Best part is an entire section dedicated to explain the entire P2P lending process along with a very detailed FAQ.

Have I invested in Mint yet? No, I do not have enough spare money lying about, just yet. But I will invest here soon enough. Should you invest in it? If you have some money to spare and are not risk averse, have a decent enough credit score, yes, you definitely should.

If you would want to get a Rs. 250 voucher when you sign up for CRED, please do let me know in the comments. The referral links stay active only for 48 hours, hence can’t post a permalink here.

Please let me know of your thoughts on CRED Mint’s P2P scheme. To read in detail of the intricacies of P2P lending, this page from cleartax is a great resource. Please check it out here.

Update: Owing to RBI Guidelines, this card is currently suspended. There is hope that it shall return once the guidelines become relaxed or some other format of the part payment scheme may return. Until then, we will miss this card and its amazing concept. The suspension is active since 1st December 2022.

Hello dear readers,

As you may have read in my previous post on credit cards, I do own a few cards. I use them for specific purposes, the AMEX card to gain the rewards, ICICI-Amazon card to get cashback on Amazon, ICICI-HPCL card for some fuel related cashbacks, HSBC Platinum card since it is lifetime free and has occasional offers on it.

Of these cards, only the Amazon card offers me an option for No cost EMI for 3/6/9 months, on selected products, only on Amazon. What if, there was a card, which would provide us with a similar no cost EMI option for all spends? I feel it would be brilliant.

A few days ago, I watched a video on Youtube describing the Uni 1/3rd card. The USP of this card is that it lets you choose to split your bill on each spend, whether you want to pay it in full or convert it into a no cost EMI for 3 months. This appealed to me greatly. For the relatively big ticket spends, they can now be converted into more affordable packets for a period of 3 months, and that too is not restricted by a website or platform as such. Off course, most of the other cards offer the option to convert a big spend into EMIs but there is always an interest rate attached to it, which is not the case here for the three months period. Also, if you choose to pay the bill in full, there is a 1% cashback. 1% may not sound a lot, but it is worth the amount in actual rupees, which is in turn almost 4 to 5 times more in worth than each reward points earned. Also, the card is Visa powered, hence, no issues with acceptance. So, convinced that this is a good idea, I applied for the card.

The application process is simple enough. You download the app and sign up for a new card. A quick KYC based on your PAN card, Aadhar Card and a selfie later, you have the card assigned to you with a fair credit limit. It took about 24 hours for me to have the card available online for transactions and in a week, the card arrived home.

The box was nice and the card is minimalistic. In the box, there was the card, a mask, a bag tag and a small packet of Toblerone chocolate. Overall, a simple yet thoughtful gesture towards initiating a new customer into the fold.

The card and the goodies

As of now, I am looking forward to using this card mainly for the transactions which generally do not yield much points or cashbacks, so that the advantage of the card’s 1% cashback can be utilized.

Also, the card and its app are in beta stage, simply put, it is still a very new card, so a lot more facilities and uses of the card is expected soon. If you apply for the card now, you’ll be one of the early adopters of the card, and that is rewarded by Uni by not charging the joining or annual fee. This may change in the future though.

Finally, in my opinion, this card provides a good proposition towards owning and using a credit card. Off course, like all cards, always ensure that you are able to pay your dues in full. What makes this interesting is that if you pay in full, which you are expected to anyway, you get 1% cashback, so, that is an incentive to pay in full. And if you are just not able to accommodate the full payment or feel a little stressed about the big purchase that you have done, split the bill into 3 parts and pay with relative ease. I would recommend this card to people who have a financial discipline in place and know how to handle their finances. It is easy to overspend when you are paying just a fraction of the cost immediately. So, good luck with using this promising card and I am hoping that more facilities are made available soon.

Feel free to put up thoughts and questions as comments to the post.

First, we begin with what a time lapse video is. This is a video of a span of time which is compressed to a few seconds or minutes to observe a slow change in the setting. The best examples of time lapse videos (commonly called as simply timelapse) are the ones which show the making of huge structures or those of a day transitioning to night and vice versa.

Next, how do we make one. Timelapse are basically made of multiple photos, taken over a long period of time, and then stitched back together to make a video. The speed of the video is set in such a manner so that the video appears to be fluid and the resultant time of the video becomes a few seconds.

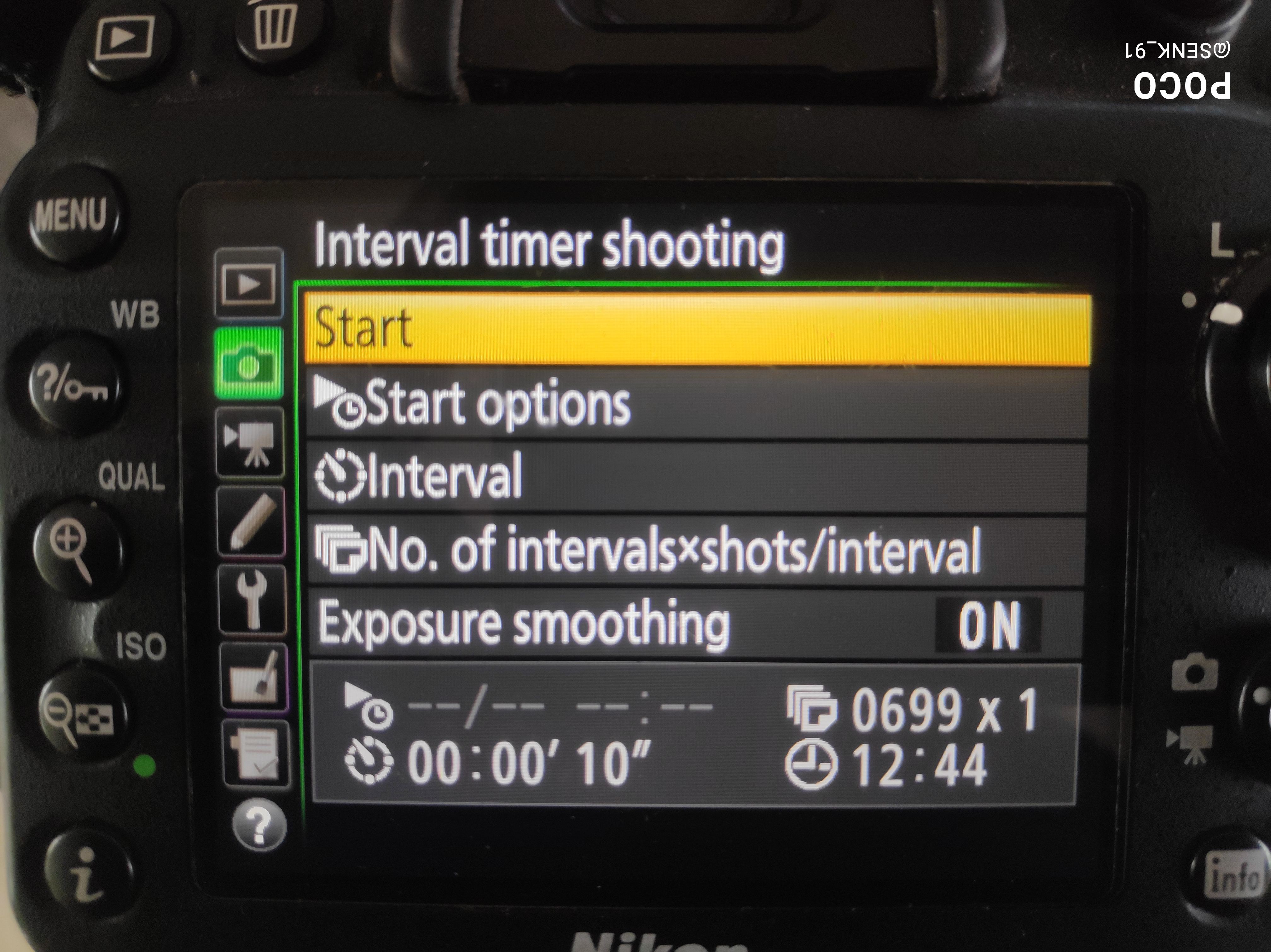

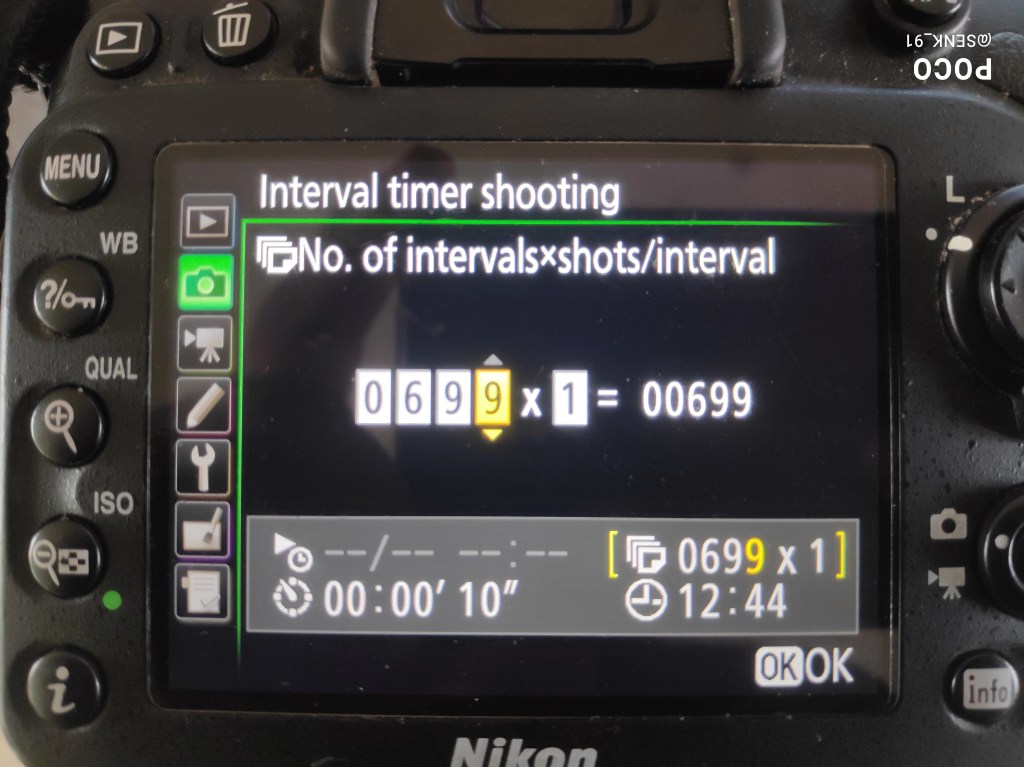

For this to be done, we need a device which is capable of taking photos at a fixed interval. So, either a camera with built in option for interval shooting, or an intervalometer which can be coupled with the camera. Below are some photos and their explanation. The camera being used here is a Nikon D7200.

Photo Shooting Menu In Nikon D7200

Interval Timer Shooting option

The photo above shows a setting where 699 photos shall be taken, with a 10 second interval between them. So, total exposure time is 6990 seconds. The setting can be done as shown in the below photos.

Interval timer shooting submenu

Interval timer shooting submenu 2

One sets the time interval between each shot, while the other setting is used to determine the number of intervals and number of photos in each interval.

One should pay attention to the fact that using these settings you can change only the number of photos being taken, not the photo’s settings. So, the ISO, Aperture, Shutter Speed and Focus has to be set by the user first.

Once the number of photos are taken, they must be processed to produce a timelapse video. There are multiple options to achieve this. Quick google searches lead to many paid and free options easily and the instructions are quite straightforward.

A calculation must be understood here. The relation between the number of frames and resultant video.

In the case we have here, we have a total of 699 frames, over a span of 6990 seconds. For a smooth video, it must be played back at about 30 fps (frames per seconds). So, my resultant video is going to be approximately, 699/30 = 23.3 seconds long. So, I shall be representing 6990 seconds, i.e almost 2 hours worth of exposure in about 24 seconds.

Add a music to the video which is fitting to it, and Voila! You have your timelapse! Check out the one I made using the settings explained above.

Timelapse video of a seedling unfurling

Offcourse there are apps available now in which all you must do is set the phone at a particular location, dial in the time you want the resultant video to be, or the exposure time, and once the exposure is done, the app returns you a expertly made video. In fact, some DSLRs also come with this option of inbuilt timelapse. Mine comes with the interval timer option only. Anyway, I hope the post is useful to anyone who wants to know about the wonderful thing a timelapse is.

Feel free to let me know of your thoughts in the comments below.

There is a tiny chance that by now, you have never heard of Bitcoin. If not, do a quick wikipedia search and come back here. I will carry on with the premise you know what the Bitcoin is and also assume that you did not manage to amass it while it was still possible for a normal salaried person. I miss not being able to grab that opportunity.

So, just like I did with rushing with the NFT opportunity, I was elated when a friend invited me to the Pi Network.

Now, the Pi network is currently in a nascent stage, beta stage, if you may call it, where the pioneers mine the coin (Pi Coin) on their mobile phones using their mobile app. Recently they launched a non custodian wallet too and gave us 100 test pi coins to test out, which works just fine. The core team does plan to launch the mainnet and the coin into the public exchange by the end of 2021, a time when the coins will have some real value in terms of fiat currency. Till then, honestly it is still make believe.

What strikes strange, is the way the network is being marketed, where one has to be invited to be able to join the network and then as he/she adds more people to the network, the speed of mining increases. It sounds absolutely like a multi level marketing scam, except there is no money involved. There is an app which you must download and run. The app has a tiny battery footprint, uses minimum data, does not ask for permissions of storage, location, phone or messages. It asks for contacts permission for inviting others, which can be denied without affecting the functioning of the app. For mining to happen, the user must register and put in an attendance, once every 24 hours, maybe watch 1 or 2 ads and that’s it.

This has every smell of a scam and my brain says that it is, but the heart says, what if the the core members are not scamming us after all? What if this explodes like the bitcoin? Didn’t you hear stories where the early adopters of Bitcoins were called loons and fools? What is the risk anyway? There is no money involved and we provide our life’s data to google and facebook anyway to be used as a product, so what’s the harm?

For me, as long as there is no actual money from my pocket is on the line, I am a 100% ready to try out a new product. If, down the line they ask us for money, hard real money, then shall I decide, whether I want to continue or not.

Till then, I shall keep mining this coin.

Since you cannot join the network without an invite, you can use my code after you sign up : novemberking91

I wish that you take this leap of faith and that our collective leaps are rewarded. Its not completely wishful thinking though, there are multiple websites and pages which are coming up discussing about this new coin, Pi. Do check them out and do decide, just do remember, in case this hits the market good, and the values go up high, on 28th of April 2021, you had been shown the possibility of it, yet again!

This post is in no way containing all the data that is to be known about the coin, but it tries to get you, dear reader to have an interest in the matter. I hope I was able to do it.

Good luck to all of us.

Cheers!!

The photo of the Pi coin is not mine. I took the photo from this link and have added the texts on it.